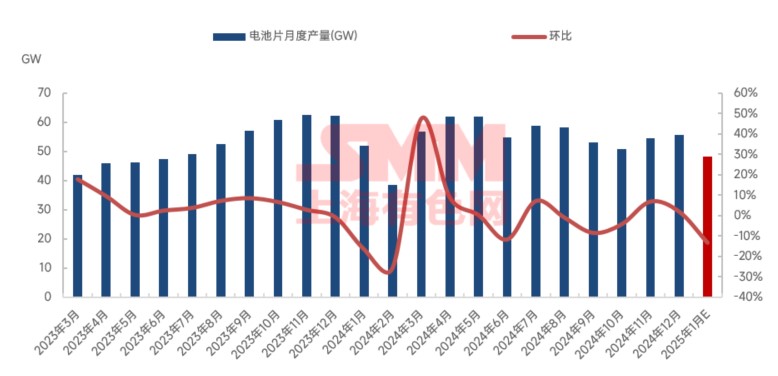

The 2025 Chinese New Year break schedule has been released. Except for battery manufacturers that have ceased production, most battery bases plan to rotate shifts during the holiday, with production lines continuing operation without shutdowns. A few battery manufacturers will halt production for three weeks for line repairs, maintenance, and upgrades during the holiday, but the overall impact on supply is relatively small. The more significant impact comes from the production cut plans of leading semi-integrated and integrated battery enterprises. In January 2025, battery production cuts amounted to 7.36 GW, with the top three companies accounting for nearly 80% of the reductions.

According to the SMM survey, the planned production of solar cells in January 2025 was 48.13 GW, including 3.42 GW of P-type cells and 44.74 GW of N-type cells, down 13.3% MoM. The decline in January production was mainly due to the Chinese New Year holiday, compounded by labour shortages and logistics constraints, leading to a downturn in both upstream and downstream demand.

Among the 60 companies that had achieved large-scale production in January, 13 remained in a state of shutdown. During December 2024-January 2025, 1-2 companies resumed production after shutdowns, and 1-2 battery manufacturers are expected to resume production after the Chinese New Year. Battery production in February 2025 is expected to remain largely stable.

By manufacturer type, the January production schedule for integrated and semi-integrated manufacturers totaled 34.06 GW, including 2.12 GW of P-type cells and 31.93 GW of N-type cells, down 15.69% MoM. Specialized battery manufacturers scheduled 14.07 GW, including 1.30 GW of P-type cells and 12.7 GW of N-type cells, down 6.94% MoM.

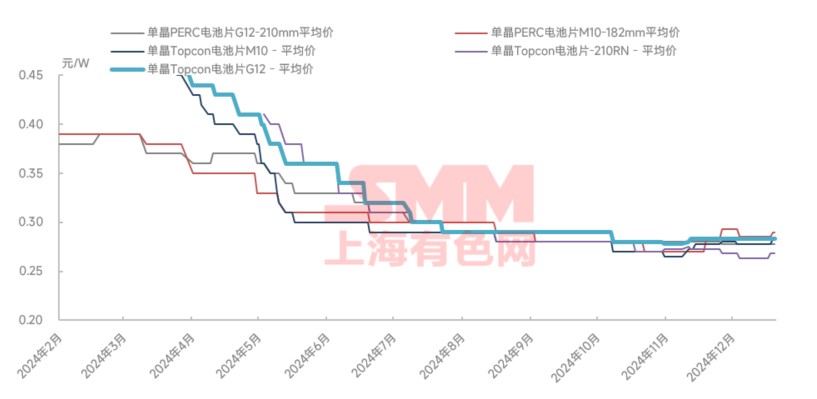

By technology type, domestic PERC cell production in January decreased by 15.57%, Topcon cell production decreased by 14.35%, HJT cell production decreased by 11.36%, while BC cell production remained largely stable.

By size, the reduction in PERC cell production was mainly in the 182 size, with other PERC sizes already discontinued. Topcon cell production cuts were primarily in the 210R size and other non-mainstream sizes (proprietary sizes of integrated manufacturers were gradually discontinued). The 183-series cells saw slight production cuts, while the 210N cell production increased against the trend. HJT cells were predominantly in the 210 half-cut size.

It is well known that the recent solar cell market has been on the rise, with prices increasing. This is partly driven by the rising silicon wafer prices, which strengthened cost support, and partly influenced by market sentiment. In December, industry self-discipline sentiment surged, module prices rose, and manufacturers voluntarily initiated production cut plans, effectively managing inventory on the supply side. In 2025, leading battery manufacturers spearheaded production cuts and price hikes, with orders showing signs of spillover. Other first- and second-tier battery manufacturers experienced sufficient demand, jointly refraining from price cuts, and prices of all types of solar cells increased. At the end of December and early January, downstream module manufacturers stockpiled batteries, further supporting solar cell demand.

We expect the likelihood of solar cell production cuts in February 2025 to be relatively low, with production levels likely to remain largely stable. On the price side, strong cost support is expected. Although no demand increase is anticipated in February, the strong cost support for batteries suggests prices may remain stable with an upward trend.

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)